In short

In private markets, fund accounting records how a fund's economics are split between the firm that manages it and the investors who back it.

Three things make the private-markets version hard: every figure has to be allocated across many investors, distributions run through a waterfall that decides who gets paid and in what order, and a single fund is usually built from dozens of linked legal entities that all have to reconcile.

On this page

- What is fund accounting?

- Fund accounting vs standard company accounting

- Fund accounting vs fund administration

- What fund accounting involves in private markets

- How fund administrators' needs differ from fund managers'

- Why generic accounting software falls short

- Frequently asked questions

A private markets fund is a pool of capital raised from investors, the limited partners, and run by a manager, the general partner. Fund accounting is what keeps that pool accurate and accountable. It records what each investor committed, what has been called from them, what the fund owns, what it is worth, and what each investor is owed. The fund is the accounting entity, but the real work sits one level down, at the individual investor's capital account.

It applies across the full range of private markets vehicles, from buyout, venture, growth and private credit to real estate and infrastructure funds, and whether a fund is a closed-end, drawdown structure or one of the open-ended, evergreen and semi-liquid vehicles now raised to reach a wider investor base. The mechanics that follow are most demanding in closed-end funds, but the core task, allocating every figure to individual investors, holds across all of them.

That is the line separating it from ordinary corporate accounting. A company's books answer to one business. A fund's books answer to the fund and to every investor inside it at once, each with their own commitment, their own fee terms and their own running balance.

Fund accounting in private markets tracks capital, not just transactions.

A finance leader moving from a corporate role into a fund often expects the work to be familiar, but it rarely is. Corporate accounting measures the performance of one trading business over a year. Fund accounting measures the position of every investor in a vehicle whose whole purpose is to call money, invest it, and hand it back over a decade or more. The outputs, the audiences and the sources of difficulty barely overlap.

Fund accounting is the work of keeping a fund's books: recording capital calls and distributions, valuing the portfolio, calculating NAV and maintaining each investor's capital account. Fund administration is a broader service that covers this accounting and adds the surrounding operational work, including investor servicing, transfer agency, regulatory and tax support, and anti-money-laundering checks.

A manager can keep this work in-house, with its own finance team and systems, or outsource it to a third-party fund administrator that keeps the books, processes the calls and distributions, and produces investor statements on the manager's behalf. A fund administrator often provides further confidence to investors, through the point that the books are being maintained by an independent 3rd party.

Many managers do both, keeping the investment-level books close while handing investor servicing to an administrator, who will hold the responsibility for publishing the accounts. The GP will shadow, maintain a check on the fund administrator. Either way, the accounting still has to be done, and to the same standard.

Five jobs make up the core of the work. Each is harder than its name suggests, and what follows is a high-level view: every one of these areas carries real-world nuance well beyond a single article, down to the detail of how a single fee or allocation is calculated.

Capital calls

Investors commit their capital at the outset but contribute it only as the fund needs it. The general partner draws it down deal by deal through a capital call, issuing a drawdown notice that typically allows about ten business days to pay, with each investor contributing in proportion to its commitment. The accounting tracks three moving figures for every investor at once: the amount committed, the amount called to date, and the uncalled balance still available to the fund, known as the dry powder.

The pro-rata split is rarely as simple as it sounds. Investors can have the right to opt out of a particular deal, for instance where a holding creates a legal or regulatory conflict; once an investor sits out, later calls allocate it more than its pro-rata share so that it catches up and still deploys its full commitment, which means the call ratios shift with every drawdown.

Recycling adds a further layer, allowing distributions made within a defined period to be added back to commitments and the cash called again.

Management fees complicate the picture further as they move to deal-based calculations, which become intricate when investors hold positions across several funds and carry their own negotiated terms, and the same applies to fund expenses. Late closers must also be brought in, typically by paying equalization interest to the investors who committed earlier.

Distributions and the waterfall

When the fund sells an investment or receives income, the proceeds flow back out through a distribution waterfall. The waterfall is the set of rules in the partnership agreement that decides who is paid, how much, and in what order. It is where carried interest is actually determined, and it is the calculation most likely to be wrong in a spreadsheet.

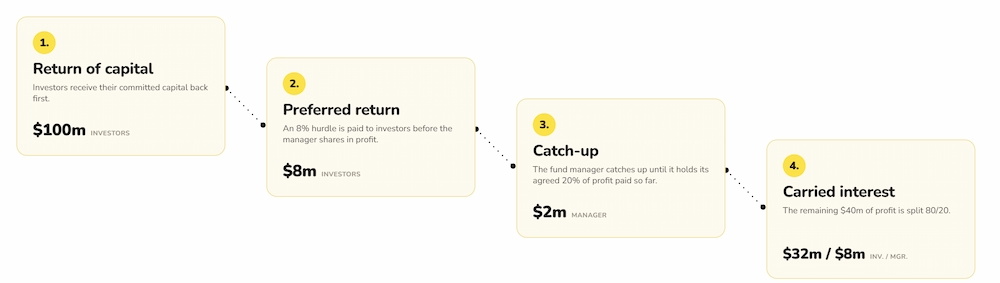

A worked example makes it concrete. Take a fund that invested $25m in a single company and sells it for $50m, a $25m profit. On a deal-by-deal basis the manager can take carry on that profit as soon as the deal is realized, without waiting for the rest of the fund's capital to be returned. The waterfall runs in four tiers.

- Return of capital. Investors receive the $25m invested in the deal back first. $25m of profit remains.

- Preferred return. Investors receive a preferred return, here an 8% hurdle worth $2m, before the manager shares in any profit. $23m remains.

- GP catch-up. The manager then receives a run of distributions until it holds its agreed share of the profit paid so far. At a 20% carry that catch-up is $0.5m. $22.5m remains.

- Carried interest split. Everything left is split 80/20. Investors take $18m, the manager takes $4.5m.

The investors end with $45m and the manager with $5m, and that $5m is exactly 20% of the $25m profit. Because the manager is paid on this deal before the rest of the fund's capital is returned, a clawback applies at the end of the fund's life to recover any carry that later losses show was overpaid.

That example is an American, or deal-by-deal, waterfall: the manager takes carry as individual deals succeed, which pays it sooner and relies on a clawback to return any overpaid carry at the end of the fund's life. A European, or whole-fund, waterfall instead returns every dollar of capital and preferred return across the entire fund before the manager sees a cent of carry. The mechanics differ enough that getting the model wrong can misstate carry by millions, which is why purpose-built systems run it as an Embedded Waterfall rather than an offline spreadsheet.

NAV calculation

A fund's net asset value is the fair value of everything it holds, less its liabilities. In public markets that is almost mechanical, because prices are quoted. In private markets it is the hard part, because most holdings are private companies with no market price. Valuation teams estimate fair value under IFRS 13 or ASC 820, using comparable company multiples, discounted cash flow, or the price of a recent funding round, and they do it every quarter. NAV per investor then differs across the register, because investors entered at different times and pay different fees. One fund, one headline NAV, and as many investor-level NAVs as there are capital accounts.

Investor allocations and carried interest

This is the engine room. Every economic event the fund experiences has to be allocated to investor capital accounts in the right proportions: management fees, which may vary by investor class or side letter; fund expenses; realized and unrealized gains; and the waterfall outcome itself. Carried interest, the manager's share of profit, is the most scrutinized number of all. It is sized in the waterfall, tested against the preferred return, and often subject to a clawback if early distributions paid out more carry than the fund's final performance justified. Allocations are not a year-end exercise. They move every time capital does.

Multi-entity fund structures

A fund is rarely a single legal entity. To serve investors in different countries and tax positions, managers build structures: master-feeder arrangements, parallel funds, blocker corporations for tax-sensitive investors, and special purpose vehicles for individual deals. Each entity keeps its own books, and the fund accountant has to keep all of them correct and then consolidate the whole into one coherent position. The updated ILPA Reporting Template, in force for funds in their investment period from the first quarter of 2026, now asks feeder funds to report their own costs alongside their share of the master fund's, raising the bar again. Complexity does not add across these entities. It multiplies.

A fund manager runs the books for its own funds and knows them intimately. A fund administrator runs the books for many managers at once, which provides different challenges.

The administrator's first duty is separation. Every client's data has to be walled off from every other client's, with no risk of one fund's figures bleeding into another's. The second is repeatability: the same close process run cleanly across dozens or hundreds of funds, with different structures and different terms, every quarter, on time. The third is the audit trail, because each client's auditors and regulators will test the work, and the administrator has to show how every number was reached.

A manager can tune its operation deeply for one set of funds. An administrator has to industrialize breadth and control across many, which is why fund administration software built for a single fund tends to buckle the moment it is asked to serve a book of clients.

General-purpose accounting tools are built for one company with one chart of accounts. They have no concept of a limited partner, a commitment, an uncalled balance, or a waterfall. Asked to run a fund they cannot, so the gaps get filled with spreadsheets, and of everything a fund does, fund accounting resists automation longest, because the logic lives in bespoke partnership terms rather than standard rules. The spreadsheets that fill the gap hold no real audit trail and break quietly at scale, and the workings of a billion-dollar fund end up living inside one person's head.

Purpose-built private equity accounting software models the fund's economics natively instead. LemonEdge runs an event-driven accounting engine: every economic event, a call, a valuation, a distribution, generates its own ledger entries and investor allocations automatically, with the audit trail attached rather than rebuilt after the fact. Automating fund accounting this way changes what the books are for. They stop being a record you defend once the quarter closes and become one you can trust while it is still open.

What is fund accounting in private equity?

It is the accounting used to track a private equity fund's capital and split its economics between the manager and its investors. Every capital call, fee, gain and distribution is allocated to individual limited partners according to the fund's partnership agreement, rather than rolled up into a single company's accounts.

Is fund accounting only for nonprofits?

No. The same term is used in the charity and government world, where it means earmarking money by purpose, which is why so much online material points there. In private markets it means something different: tracking investor capital and returns inside a fund, whether a closed-end structure or an open-ended, evergreen one. This guide covers the private-markets meaning.

What is the difference between fund accounting and fund administration?

Fund accounting is the activity of keeping the fund's books. Fund administration is the outsourced service of doing that work, plus investor servicing, transfer agency and regulatory support, on a manager's behalf. A manager can do its fund accounting in-house or hand it to an administrator.

What does a fund accountant do?

A fund accountant processes capital calls and distributions, allocates fees and gains across investor capital accounts, calculates NAV, runs the distribution waterfall, prepares investor statements and reporting, and supports the annual audit. In private markets the role leans heavily on understanding fund structures and partnership terms, not just bookkeeping.

What software is used for fund accounting in private markets?

Specialist platforms built for fund economics, rather than generic corporate ledgers such as QuickBooks or Xero, which cannot model commitments, allocations or waterfalls. Many firms still patch older systems with Excel; purpose-built fund accounting software removes that dependency by handling allocations, NAV and waterfalls inside one system.

About the author

Gareth Hewitt is co-founder of LemonEdge, the fund accounting and operations platform built for private markets. Gareth spent over 20 years in the industry, frustrated with no one truly delivering the solutions to the increasing complexity of private markets.