In short

A distribution waterfall is the contractual order in which a private equity fund pays out proceeds. Limited partners recover their capital and a preferred return before the general partner catches up and takes its share of the profit, typically an 80/20 split. Spreadsheets struggle with this because the rules are specific to each fund's LPA, they stack on top of one another, and they change every time the agreement is amended. Automating the waterfall means encoding those rules once, in software that runs the calculation and keeps a full audit trail behind every figure. It is achievable, and most funds operating at scale have already moved.

What is a distribution waterfall?

A distribution waterfall sets the priority of payments when a fund returns money to its investors. It exists because limited partners and the general partner do not share proceeds equally or at the same time. The LPA defines a sequence, and cash flows through it in order, with each level satisfied before the next receives anything.

Two structures dominate, and the difference matters more than most software demos admit. A European waterfall, sometimes called whole-of-fund, withholds carried interest from the GP until investors have received all of their contributed capital and their preferred return across the entire fund. It is the more LP-friendly model and the more common one in institutional funds today. An American waterfall, also called deal-by-deal, lets the GP earn carry on individual realizations as they happen, before every dollar of fund-level capital has been returned. It rewards the GP earlier, which is why it usually carries a clawback provision so that LPs can recover overpaid carry at the end of the fund's life if early winners are followed by later losses.

Most real funds are not purely one or the other. Hybrid structures borrow features from both, layering hurdles, catch-up rates, and clawback mechanics in combinations written specifically for that fund. That specificity is the whole problem, and it is the reason a generic calculation engine rarely survives contact with an actual LPA.

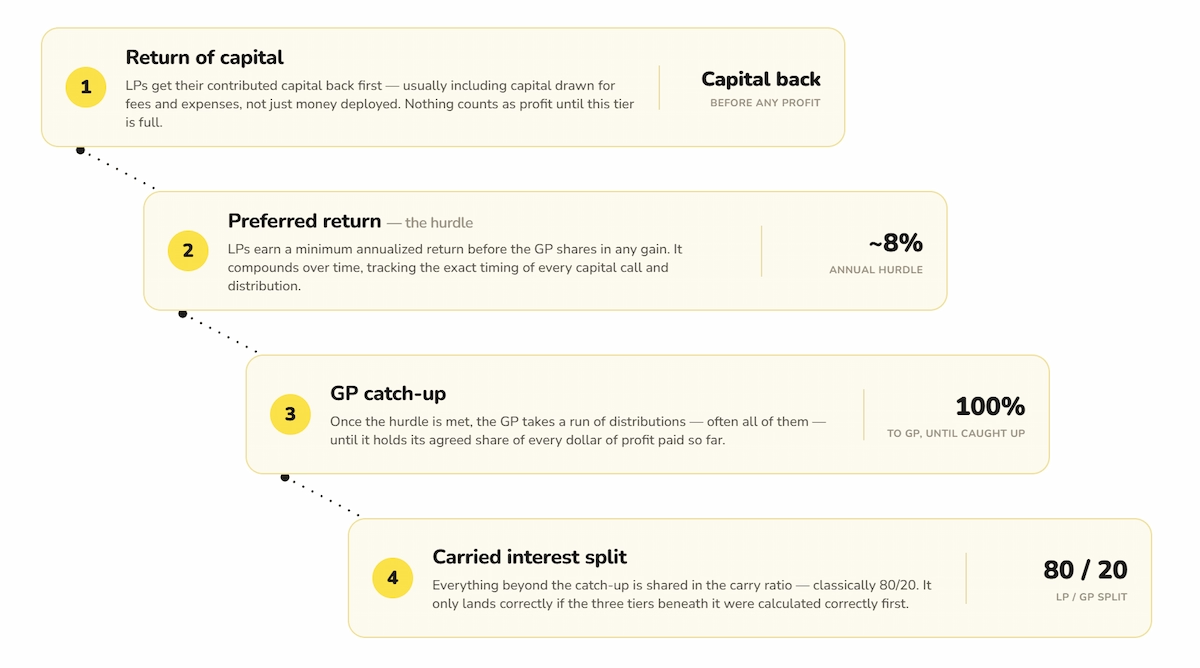

The four tiers, step by step

Whatever the structure, the mechanics resolve into four tiers. The labels are standard even when the percentages are not.

- Return of capital. Investors get their money back first. The fund returns contributed capital to LPs, and in most agreements this includes capital drawn for fees and expenses, not only capital deployed into investments. Nothing is treated as profit until this tier is full.

- Preferred return (the hurdle). Before the GP shares in any gain, LPs receive a minimum annualized return on their capital, conventionally 8%, though it is negotiated fund by fund. The hurdle compounds over time, which is the first place spreadsheets quietly drift, because the accrual depends on the exact timing of every capital call and every distribution.

- GP catch-up. Once the hurdle is met, the GP receives a run of distributions, often 100% of them, until it has earned its agreed share of the profit distributed so far. A full catch-up trues the GP up to its carry percentage on all profit, not only the profit above the hurdle. The catch-up rate is one of the most heavily negotiated terms in the LPA and one of the easiest to model incorrectly.

- Carried interest split. Everything beyond the catch-up is shared in the carry ratio, classically 80% to LPs and 20% to the GP. This is the tier people picture when they say "carry," but it only behaves correctly if the three tiers beneath it were calculated correctly first.

The numbers make it concrete. Take a fund where LPs contribute $100M and the investment returns $150M in total proceeds. Assume an 8% hurdle that has accrued to $20M over the holding period, a 100% GP catch-up, and 20% carry.

The GP ends with $10M, which is 20% of the $50M of total profit, exactly what the carry was meant to deliver. The catch-up is what gets it there. Remove it, or set its rate wrong, and the GP's economics move by millions on a single deal. That is the calculation an automated engine has to get right every quarter, across every fund, without a person rebuilding the formula each time.

Why Excel fails for waterfall calculations

Spreadsheets did not fail because finance teams are careless. They fail because a waterfall is a poor fit for the tool, and three structural weaknesses show up at scale.

One is fragility. A waterfall model is a dense web of linked cells and nested formulas, and a single broken reference, or a row inserted in the wrong place, can misstate carried interest without throwing any visible error. Version control is the next problem. When the model lives as a file, the definitive version is whichever copy happens to be open, and reconciling two analysts' edits at quarter-end becomes its own source of risk. Then there is the audit trail, or the lack of one. A spreadsheet records the result and not the reasoning, so when an LP or an auditor asks why a figure landed where it did, the answer tends to depend on whoever built the file still being around to explain it.

These weaknesses are getting more exposed, not less. The updated ILPA Reporting Template, released in 2025 and effective for funds in their investment period from the first quarter of 2026, removed the optionality that previously let GPs report at a coarser level of detail. It now requires a single, uniform level of granularity, including on carried interest. A manual process built for the looser standard does not quietly scale to the stricter one. It breaks, and it tends to break at the close, which is the worst possible moment.

How automation handles it

Automation does not mean a faster spreadsheet. It means moving the rules out of cells and into a system that treats the waterfall as logic rather than arithmetic.

An automated engine encodes the terms of the LPA directly: the hurdle, the compounding basis, the catch-up rate, the carry split, and the order in which they apply. Once those rules are defined, the system applies them to every distribution automatically, recalculates when capital is called or returned, and produces the same answer every time from the same inputs. Because the calculation is governed inside the system, every figure carries its working with it, which is what turns a quarter-end number into one a CFO can sign off and an auditor can trace.

There is a deeper reason the calculation belongs inside the accounting system rather than beside it. Traditional calc-only engines sit on top of the accounting platform: they load all of the accounting data in, run the waterfall, and hand back a result, but they leave no real place to store the adjustments that every close depends on. The data lives in one system and the calculation in another. When the waterfall runs inside the accounting software itself, it sits where the data already is, so the adjustments that feed it can be maintained correctly and in one place rather than reconciled back across a bolt-on black box.

This is the gap Embedded Waterfall was built to close. Rather than abstracting the waterfall into a black box, it applies each fund's specific LPA rules transparently, so the logic that produced a given carry figure stays visible and reviewable rather than buried. The harder structures are where this matters most: multi-level fund-of-funds arrangements, carry-linked entities, and the layered hurdles that hybrid waterfalls create. Those are precisely the cases a spreadsheet handles worst and an LPA most often contains.

For teams scoping this for the first time, it helps to be clear on what fund accounting involves in private markets before deciding which parts to automate first, and to see where the waterfall connects to the rest of the close through the broader private equity fund accounting software underneath it. The question is no longer whether the waterfall can be automated. It is how long a fund can keep signing off carry from a file that only one person fully understands.

FAQs

How do you automate waterfall distributions?

You encode the fund's LPA terms, the hurdle, the catch-up, the carry split, and the order of the tiers, into fund accounting software that applies them to every distribution automatically. The system recalculates as capital is called and returned, holds an audit trail behind each figure, and reproduces results on demand, which removes the manual model rebuild that spreadsheets require every period.

What is the difference between American and European waterfall structures?

A European, or whole-of-fund, waterfall pays the GP carried interest only after LPs have recovered all of their capital and preferred return across the entire fund. An American, or deal-by-deal, waterfall lets the GP earn carry on individual exits sooner, usually with a clawback so LPs can recover any overpayment at the fund's end. European is more LP-friendly and more common institutionally.

Can fund accounting software handle complex carried interest calculations?

Yes, and complex carry is the main reason to use it. Purpose-built engines model full catch-ups, tiered hurdles, clawbacks, and carry-linked entities that spreadsheets struggle to track reliably. Because the rules are defined once and governed in the system, the carry figure stays consistent and auditable even as fund structures grow more layered.

Why is Excel risky for waterfall calculations?

A waterfall model in Excel is a web of linked formulas where one broken reference can misstate carry with no error flag. Add weak version control and no real audit trail, and a single file becomes hard to defend to an LP or an auditor. The risk compounds as reporting standards tighten and fund structures get more complex.

About the author

Gareth Hewitt is co-founder of LemonEdge, the fund accounting platform purpose-built to simplify capital complexity. He leads the product behind how LemonEdge brings the hardest fund accounting processes, distribution waterfalls among them, onto a single auditable system rather than leaving them in spreadsheets and in doing so, building trust.

.avif)